Examining the Sensitivity of Residential Housing to Mortgage Rates

Examining the Sensitivity of Residential Housing to Mortgage Rates

Former JPMorgan Chase Global Chief Economist (Ph.D. in Economics) and Current BQ Chief Economist

Have you ever wondered why the share of new single-family home sales has been rising? The short answer is the data reveals that the sale of newly constructed homes is less sensitive to changes in U.S. mortgage rates than existing homes. One reason for this outcome is that the supply of housing units takes on added importance when mortgage rates are high and rising! Although homebuilders must pay higher rates during the construction phase for loans they take out, many have opted to stop building spec homes and only focus on homes purchased by prospective homeowners requiring high down payments to minimize their financing costs.

Source: U.S. Census Bureau and the National Association of Realtors

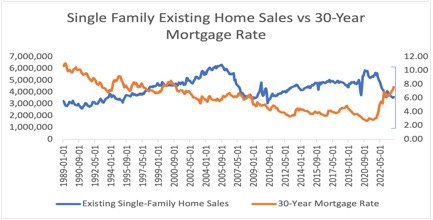

Impact of Rising Mortgage Rates

It is no secret that many existing homeowners have become reluctant to list their homes to avoid having to trade in their 5.0% or lower mortgage rates, representing 80% of all outstanding mortgages! This has resulted in a lower volume of transactions in the existing home sales market. As mortgage rates have increased, existing home sale transactions have fallen by 38%, from 5.81 million (SAAR) in January 2021 to 3.61 million (SAAR) in October 2023.

A statistical regression of housing transactions (using data from Jan. 1989 to Oct 2023) revealed that existing home sales were 9.7 times more sensitive to changes in U.S. mortgage rates than newly constructed home sales. These results explain why the surge in U.S. mortgage rates has had less of a negative impact on freshly built home sales activity.

A reluctance to list homes has kept the inventory of previously owned homes below their 6-month normal levels, reducing the number of transactions. With fewer choices available to existing home buyers, home buyers have switched to the new home sales market to satisfy some of their pent-up demand.

Source: The U.S. Census Bureau and Freddie Mac

While some have pointed out that the monthly supply of existing home inventory has increased, that metric is less accurate because it measures stocks at the current sales pace. As sales have dropped, the monthly inventory levels measured relative to sales have risen.

Source: The Federal Reserve of St. Louis and Trading Economics

A more accurate read of inventory levels can be gleaned from the total number of units available for sale. When we track this metric over time, one can see that the inventory of existing homes has been gradually shrinking!

Existing Home Sales Inventory

Source: The Federal Reserve of St. Louis and Trading Economics

Other data we examined revealed that newly constructed homes have become more competitive with existing homes. Historically, the median price premium on new home sales has ranged from 15 to 20%, but in recent months, the spread between both categories has been reduced to less than 5.0%! This has allowed prospective buyers access to additional housing inventory at a lower pricing premium.

Along with a narrower pricing spread, the inventory of newly constructed homes has also gradually increased! This has occurred because, on a relative basis, freshly built homes are less impacted by rising mortgage rates. For buyers willing to order the construction of a new home from scratch, many builders have remained eager to operate in this safer environment.

Summary and Concluding Thoughts:

The U.S. housing market has been negatively impacted by high mortgage rates, discouraging the 80% of mortgage holders with rates of 5.0% or less from listing their homes for sale; it has left pent-up demand unsatisfied. The only silver lining within this challenging environment is that as many as 40% of current homeowners own their home outright without a mortgage! Unlike those with lower-rate mortgages, this group has greater flexibility operating in a higher mortgage rate environment.

Nonetheless, it has been interesting to see that freshly built homes have gradually increased their market share of homes sold since they have historically been less sensitive to changes in mortgage rates.

The good news is that average 30-year mortgage rates have dropped by more than 100 basis points since November 2023. If the Federal Reserve keeps its promise (as implied by the central bank’s latest Survey of Economic Projections) to lower short-term policy rates by at least 50 basis points. In that case, the housing environment will continue to improve as the result could be lower mortgage rates if inflation expectations and actual inflation also move lower.

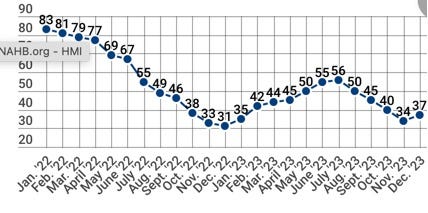

The anecdotal evidence suggests that if mortgage rates touch 5.0% to 6%, homebuilders may begin to build spec homes again and boost housing inventory levels. Perhaps as a sneak preview of what is coming, the Homebuilders Index rose in December 2023 for the first time in four months as mortgage rates have eased in the past month. Fortunately, the evidence strongly suggests that U.S. mortgage rates are likely to continue moving lower in 2024; the only question is: How much lower?

The U.S. National Homebuilders Index

Source: The National Association of Homebuilders